A window of opportunity: Qualified opportunity zone funds in 2026

Opportunity zones (OZs) were designed to unlock private investment in communities poised for growth, while delivering meaningful tax advantages to investors. As the landscape evolves, the strongest opportunity zone outcomes are increasingly concentrated in:

- Proven markets

- Proven tracts

- Proven execution

If you’re considering a qualified opportunity zone fund (QOF) investment, 2026 offers potentially significant strategic advantages.

Why invest in a QOF in 2026?

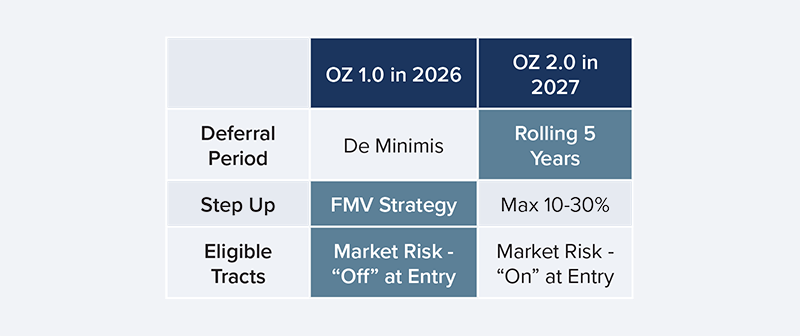

1. Today’s Fair Market Value may be tomorrow’s missed advantage.

The QOF statute requires taxation on the investment that was sold based on the fair market value (FMV) of the investment on December 31, 2026. With that date approaching, we are in a short window to obtain a valuation discount that will materially reduce taxable gain.

Specifically, between now and December 31, 2026, investors have the opportunity to capture Internal Revenue Code (IRC)-mandated valuation discounts by investing in QOFs holding assets still under construction at year-end 2026. Depending on individual circumstances, the tax value derived from the FMV discount may surpass the QOF-related tax incentives projected to be available in 2027 under the One Big Beautiful Bill Act framework that establishes OZ 2.0 rules.

Put simply: the December 31, 2026, valuation discount is a strategic opportunity to reduce taxable gain.

2. Current opportunity zone tracts are proven. Future tracts are speculative.

The opportunity zone map we know today includes areas with demonstrated investor outcomes, infrastructure momentum and real market data — not theory.

A clear example is Scott’s Addition in Richmond, Virginia: a nationally recognized transformation story where opportunity zone investment has aligned with strong demographic trends, development activity and sustained demand.

By contrast, future opportunity zone legislation may introduce:

- New tract designations with unknown fundamentals

- Unproven market performance

- Uncertain timelines and implementation risk

In short: today’s tracts have track records. Future tracts have hopes and prayers.

3. Powerful tax advantages remain a cornerstone of QOF strategy.

Qualified opportunity zone funds provide investors with:

- The potential for tax deferral on the investment that was sold

- The potential for full exclusion of capital gains tax on appreciation, subject to holding periods and program requirements

These benefits are a primary reason investors use QOF strategies to pursue long-term wealth creation while improving after-tax outcomes.

The bottom line

We believe the best opportunity zone outcomes are driven by timing, tract quality and execution.

In 2026, investors have access to:

- Today’s market entry points

- Known tracts with real performance history

- Meaningful tax advantages

- A strategic opportunity to grow wealth — and business — more efficiently

Capital Square is committed to delivering institutional-quality real estate investment solutions, including qualified opportunity zone fund strategies, with disciplined underwriting and long-term alignment.

Is it time for you to take the next step?

Connect with Capital Square to explore how a qualified opportunity zone fund may fit into your tax strategy, portfolio objectives and long-term planning.

Disclosure

Securities offered through WealthForge Securities, LLC, Member FINRA/SIPC. Capital Square and WealthForge Securities, LLC are separate entities. There are material risks associated with investing in DST properties and real estate securities including illiquidity, tenant vacancies, general market conditions and competition, lack of operating history, interest rate risks, the risk of new supply coming to market and softening rental rates, general risks of owning/operating commercial and multifamily properties, short-term leases associated with multifamily properties, financing risks, potential adverse tax consequences, general economic risks, development risks, long hold periods, and potential loss of the entire investment principal. Past performance is not a guarantee of future results. Potential cash flow, returns and appreciation are not guaranteed. IRC Section 1031 is a complex tax concept; consult your legal or tax professional regarding the specifics of your particular situation. This is not a solicitation or an offer to sell any securities. Please read the Private Placement Memorandum (PPM) in its entirety, paying careful attention to the risk section prior to investing. Private placements are speculative and illiquid. Diversification does not guarantee profits or protect against losses. FINRA Broker Check link: https://brokercheck.finra.org/.